The Biennial Survey: Reflections from Asia Public Accounts Committees two-years on

Published 30 November 2021

Exercise for Public Accounts Committee chairs, clerks and members during the CAPAC Asia Workshop, Kuala Lumpur August 2019

The Biennial Survey: Reflections from Asia Public Accounts Committees two-years on

In June 2014, the Commonwealth Association of Public Accounts Committees (CAPAC) was formed by Chairs and Members of Public Accounts Committees (PACs), and equivalent Committees of Commonwealth parliaments. One of CAPAC’s core functions was to ‘define, publish and promote standards of good practice... to assist CAPAC Member Committees in being effective, transparent and independent’.

CAPAC produced The Public Accounts Committee Principles, a list of standards of good practice to be observed by Public Account’s Committees scrutinising government spending. CPA UK consulted with Committee chairs, members and clerks to condense these Principles into nine benchmarks to be used as a self-reflection tool by members and clerks. A full list of the ten PAC Principles can be found at the end of this article.

Between 2018 and 2020, 52 Commonwealth PACs completed a self-reflection exercise based on these Principles. Committees were encouraged to rate their compliance with the principles and the responses were used to inform a series of 4 regional programmes designed for PAC Chairs, members and clerks.

Phase 2 – The relaunch of the survey

Since the start of 2021, 25 of those PACs from the Africa, Asia, and Pacific regions have now re-assed their committee against the benchmarks which includes an additional benchmark on the relationship of the committee with the Supreme Audit Institution of the jurisdiction. This benchmark examines the independence of the Supreme Audit Institution which should be firmly rooted in the Constitution or equivalent legislation and should spell out clearly the extent of its independence and powers. PACs should work to safeguard the independence of SAIs and ensure that they have the resources they need to carry out their statutory mandate. These updated results allow us to observe how their PACs have changed over the last two years.

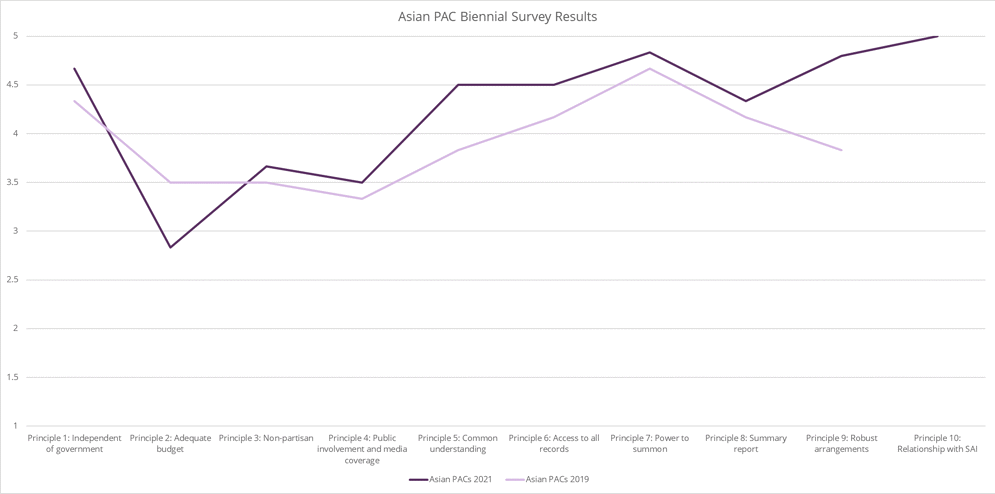

Image 1: Comparison of Asia PAC responses to the Biennial Survey in 2019 and 2021

Findings from Asia

The most recent results come from 6 Commonwealth Asian PACs, the same 6 PACs who completed the survey in 2019, thus providing for good comparison. The Biennial Survey reveals that PACs in Asia have rated themselves as improving on several principles of good practice since PACs completed the survey two years ago. Additionally, PACs have rated themselves as more compliant in all areas except for having an adequate budget.

The most significant improvement has been in a PACs ability to follow up on their recommendations, Principle 9 – Robust Arrangements followed closely by Principle 5 - Common Understanding of the PACs Mandate, Roles and Powers. CPA UK’s past experience and engagement with PACs shows that if they have robust follow-up arrangements in place, the government is more likely to give their recommendations appropriate consideration and not ignore PAC reports. The survey participants also report improvements in many other areas including operating with independence from government, having non-partisan and skilled support staff, PAC members having a common understanding of their and the PAC’s role and remit, and power to summon persons, papers and records.

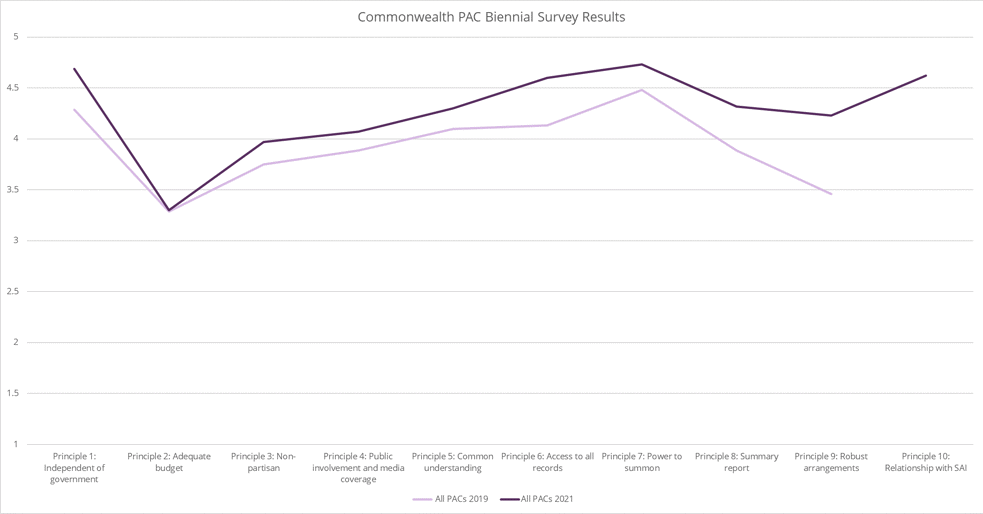

As with the 2018/2019 and 2020/2021 phase of the survey to date, the overall lowest self-rating was Principle 2: Adequate Budget. Compliance with adequate budget has declined since 2019, with over half of Asian PACs that responded reporting that their budget is currently insufficient to cover their costs. When we combine the Asian findings with the results from African and Pacific PACs, we can see a similar trend.

Image 2: Comparison of all PAC responses to the Biennial Survey in 2019 and the responses of Africa, Pacific & Asia in 2021

The self-assessment ratings against the benchmarks can also be seen in the images below. In these images, the more PACs who gave the same answer, the larger the circle, and the fewer PACs who gave the same answer, the smaller the circle.

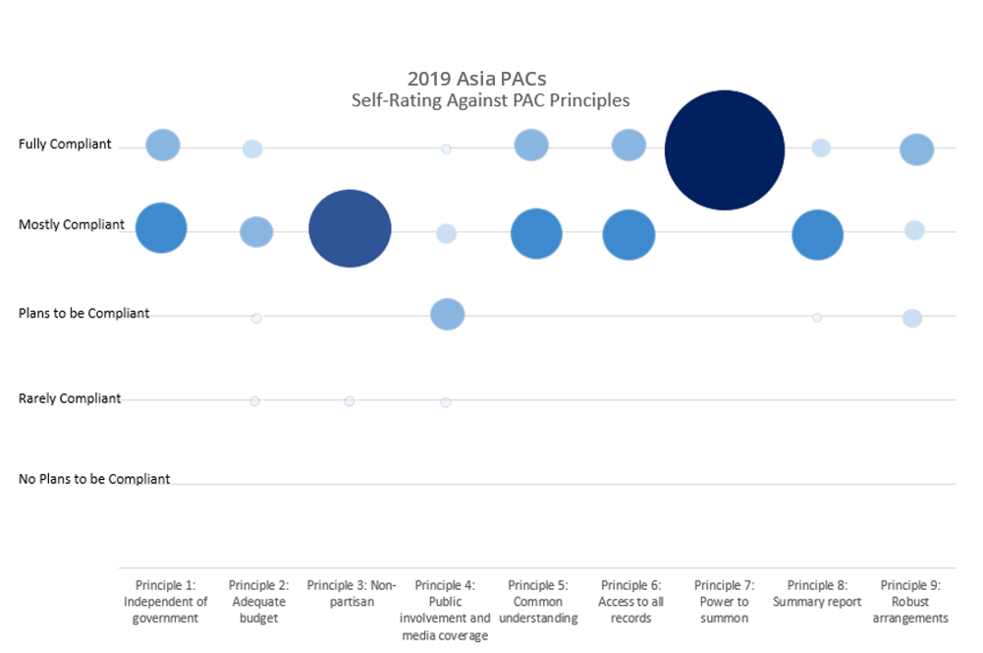

Image 3: Asia PAC responses to the Biennial Survey in 2019

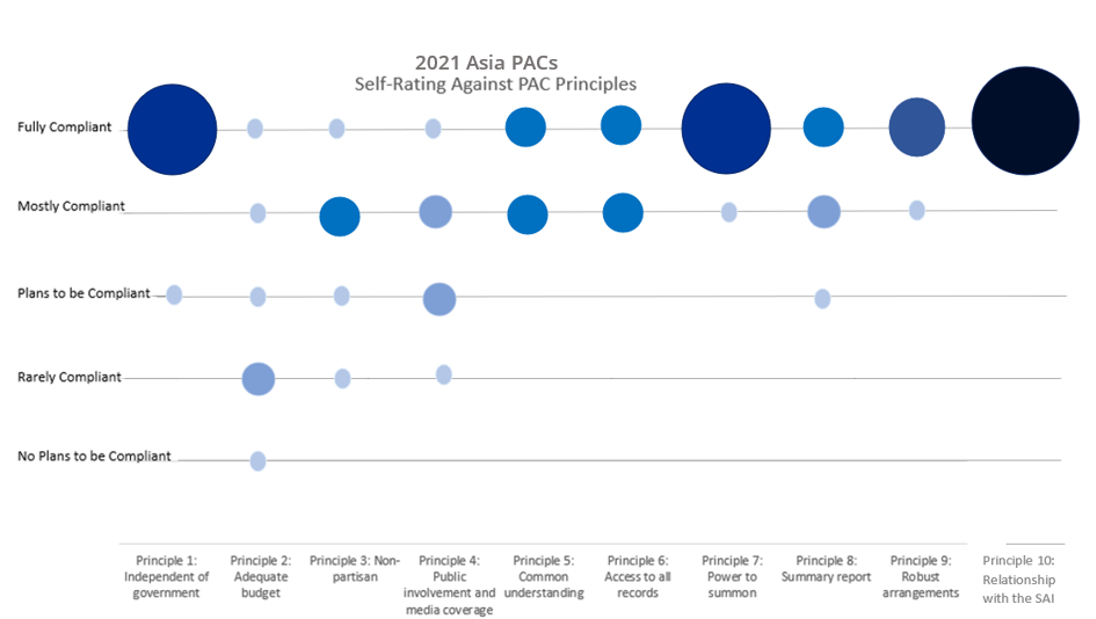

Image 4: Asia PAC responses to the Biennial Survey in 2021

For example, in 2021, all 6 PACs who answered the survey stated that they are fully compliant with Principle 10: Relationship with the SAI, hence the larger circle.

Overall, the results for 2021 show a much more varied picture than in 2019. In 2019, the majority of PACs who completed the survey rated themselves as either mostly or fully compliant with the 9 benchmarks.

However, in 2021, PACs responses are more spread out, with some stating that they are rarely compliant, have plans to be compliant, or do not have plans to be compliant with particular benchmarks. These are mostly in the areas of Principle 2: Adequate Budget, 3: Non-Partisanship, and 4: Public Involvement and Media Coverage. To determine why this is the case, further consultation with PACs would be necessary.

In 2021, all PACs who responded rated themselves as fully compliant against the newest benchmark Principle 10: Relationship With the SAI, and 5 out of 6 PACs felt as though they are most compliant against Principle 1: Independence from Government and Principle 7: Power to Summon. There is a considerable change from 2019 in which only half of the PACs who completed the survey rated themselves as fully compliant in being independent from government under Principle 1, whereas in 2021, 5 out of the 6 PACs who responded believe they are fully compliant in being independent. Improvements have also been made to Principle 9: Robust Arrangements for follow up on PAC recommendations, including timelines.

Conversely, whereas most PACs in 2019 rated themselves as being mostly compliant on Principle 3: Non-Partisanship, the results are now more varied, with results spanning from fully compliant, to rarely compliant.

Biennial Survey - Part 2

As well as asking PACs to rate themselves against the 10 benchmarks, PACs are also asked general questions about the membership of the committee, their recent hearings and reports, and their relationship with Government and the Supreme Audit Institution.

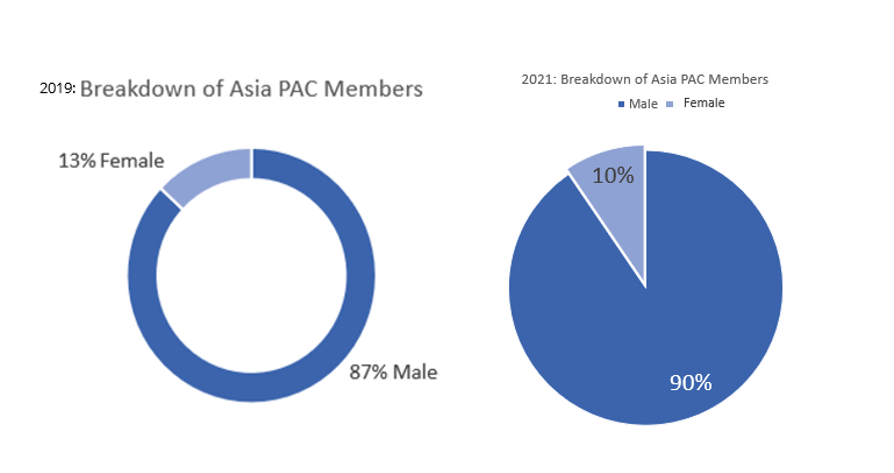

Image 5: Comparison of female representation on Asian PACs in 2019 and 2021

In terms of PAC membership, the average Asia PAC has:

- 16 members on the Committee

- 11 government members and 5 opposition members

- 14 male and 2 female members.

With an average membership of 16, Asia PACs have the largest average committee membership compared to all other Commonwealth regions.

In terms of membership, results from 2021 show a decrease in female membership of the PAC since 2019. As a result, Asia now has the lowest percentage of female representation on the PAC across the Commonwealth.

PAC Relationships

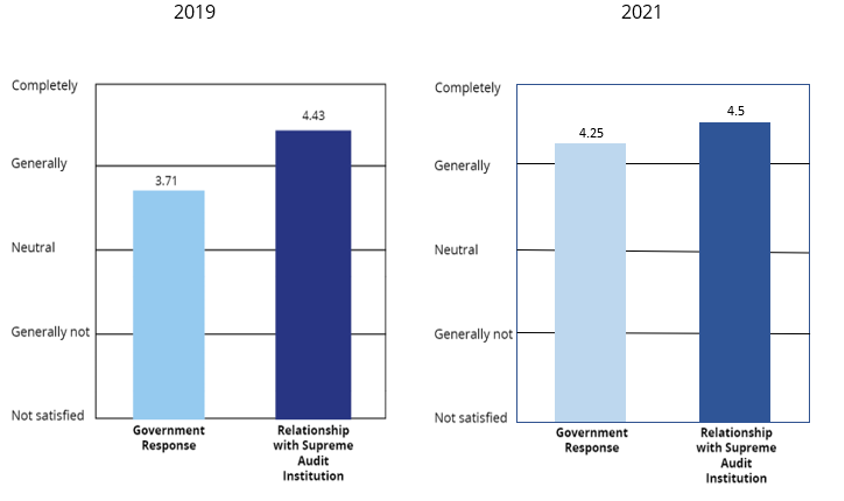

Overall, the picture is quite positive when looking at the PAC’s relationships with various stakeholders. Asia PACs have reported an increase in satisfaction from neutral/generally satisfied to generally/completely satisfied with government responses to PAC recommendations. There has also been a slight increase in the PACs satisfaction with their relationship with the Supreme Audit Institution, which was has remained in the generally/completely satisfied bracket.

Image 6: Comparison of Asian PAC's satisfaction with government responses to PAC recommendations and the relationship with the Supreme Audit Institution in 2019 and 2021

As more committees go through this self-reflection exercise over the year, CPA UK will be bringing together the data to add further comparisons, highlighting the key strengths and areas of growth for Public Accounts Committees. CPA UK uses this data in planning our future programmes and working with committees from across the Commonwealth to support each other in addressing contemporary challenges.

If these trends sound familiar to you or your legislature has experienced something different and are interested in hearing more about these benchmarks, please get in touch with us by emailing Matthew Hamilton at hamiltonm@parliament.uk

To find out more about results of the Pacific & Africa biennial surveys and to read the analysis, please click here.

Full text of the 10 Public Accounts Committee Benchmarks

- A PAC [Public Accounts Committee] should operate independently of government. PACs should have the power to select issues without government direction. The PAC’s independence should be outlined clearly through the provisions of the Standing Orders.

- PACs should have an adequate budget to cover their personnel and other operational costs, training and capacity building costs, as well as costs associated with hearings, publication of reports and sourcing external advice.

- A PAC needs non-partisan and skilled support staff. At a minimum, a PAC should have a Clerk and research staff.

- A PAC should encourage public involvement and media coverage. Committee hearings should be open to the media and the interested public, and any exceptions from this rule need to be reasonably justified.

- PAC members should have a common understanding and articulation of the PAC’s mandate, roles and powers. Members should have a good understanding of how PAC powers should be applied.

- A PAC shall have access to all records, in whatever form, to be able to scrutinise the Executive and perform the necessary oversight of public spending.

- A PAC should have the power to summon persons, papers and records, and this power shall extend to witnesses and evidence from the executive branch, including officials.

- PACs should produce a summary report of its overall findings and the extent to which its recommendations have been implemented that should lead to a debate in parliament.

- PACs need to ensure that there are robust arrangements in place to follow up their recommendations, including timelines. Such follow up may be carried out by the Supreme Audit Institution and/or the Ministry of Finance/entities concerned. However, where the PAC finds that government bodies have been slow in implementing recommendations then the senior officials of these bodies should be summoned to appear before the Committee to explain themselves.

- The Supreme Audit Institution’s independence should be firmly rooted in the Constitution or equivalent legislation which should spell out clearly the extent of its independence and powers. PACs should work to safeguard the independence of SAIs and ensure that they have the resources they need to carry out their statutory mandate.