Self-reflections from Public Accounts Committees, Two Years On

Published 31 March 2021

Exercise for Public Accounts Committee chairs, clerks and members during the Africa-UK Public Accounts Committee Workshop, Nairobi August 2018

While seen as one of the most influential and established committees in the Westminster system of parliamentary democracy, Public Accounts Committees have been replicated throughout the Commonwealth. Despite their diversity and differing contexts, they share a similar idea of what makes a ‘good Public Accounts Committee’ and many face similar challenges, from the resourcing of inquiries, engaging with stakeholders, and following up on past reports, to membership, powers and structures. Over the last two years, we have seen some improvements across committees with some noticeable regional differences.

Benchmarking Public Accounts Committees

CPA UK works closely with Public Accounts Committees to support financial scrutiny, ensuring members have the technical expertise and knowledge to hold governments to account on behalf of their citizens.

In June 2014, Chairs and Members of Public Accounts Committees, and equivalent Committees of Commonwealth parliaments, formed the Commonwealth Association of Public Accounts Committees (CAPAC). One of CAPAC’s core functions was to ‘define, publish and promote standards of good practice, in line with Commonwealth principles, to assist CAPAC Member Committees in being effective, transparent and independent’.

CAPAC produced The Public Accounts Committee Principles which include criteria to be followed by legislatures in establishing and giving mandates to their committee, as well as standards of good practice to be observed in their regular operations. CPA UK condensed these Principles into nine benchmarks to be used as a self-reflection tool by members and clerks (examining key areas for Public Accounts Committees such as independence from Government, follow-up of reports, adequate budgets - for full list see below) to rate themselves on how compliant they thought they were for each benchmark.

52 Public Accounts Committees (and equivalents) from across the Commonwealth completed this self-reflection exercise between 2018 and the beginning of 2020. These responses were also used to inform a series of 4 regional programmes designed for Public Accounts Committees Chairs, members and clerks.

Phase 2 of the Benchmarks

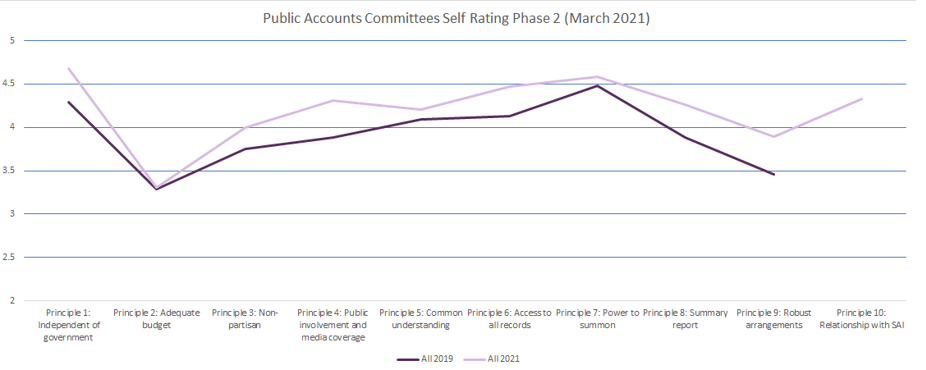

Since December 2020, 19 committees, mainly from the Africa and Pacific Region, have completed the updated survey (which includes an additional benchmark on the relationship of the committee with the Supreme Audit Institution of the jurisdiction) and reflected on progress as well as challenges the committee has faced over the last two years.

We can see that there has been some increase in compliance among the majority of benchmarks. The largest increases were with Benchmark 9: Robust follow-up arrangements (although this benchmark still remains the second lowest) and Benchmark 4: Public involvement and media coverage. A number of committees have highlighted how they have engaged with the media in a more systematic way following the Regional Series organised by CPA UK.

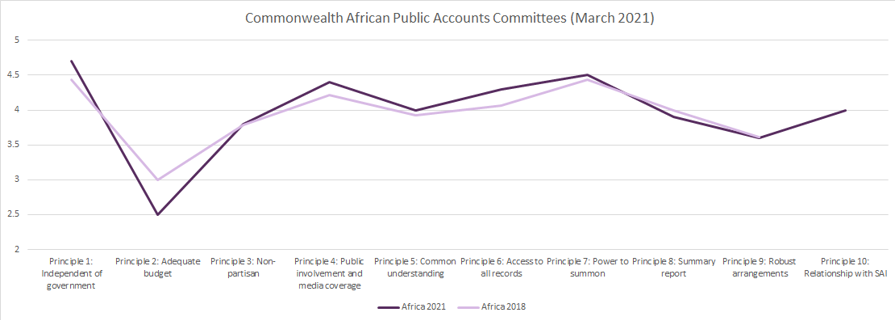

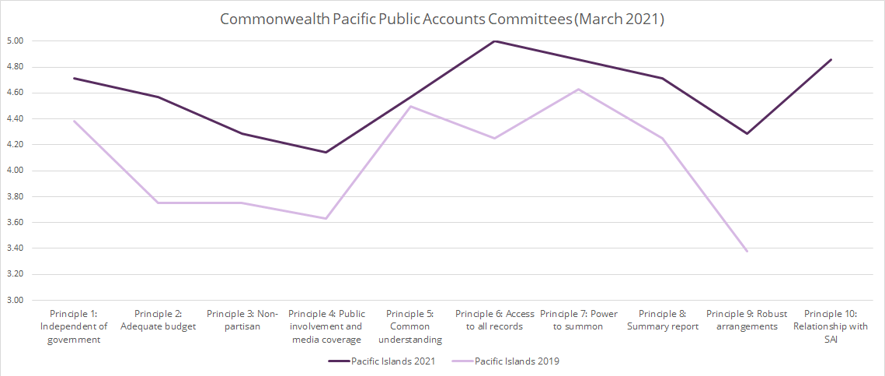

As with the first and second phase to date, the overall lowest rating was Benchmark 2: Adequate Budget which has remained stable. When we look at regional trends, we can see a slight decrease among African Committees and a slight increase in Pacific. While African Committees have overall rated themselves around the same level as 2018, Pacific Committees have seen an improvement in all benchmarks.

As more committees go through this self-reflection exercise over the year, CPA UK will be able to bring together the data to add comparisons, highlighting the key strengths and areas of growth for Public Accounts Committees. CPA UK uses this data in planning our future programmes and working with committees from across the Commonwealth to support each other in addressing contemporary challenges.

If these trends sound familiar to you or your legislature has experienced something different and are interested in hearing more about these Benchmarks, please get in touch with us by emailing Matthew Hamilton at hamiltonm@parliament.uk

Between November 2020 to March 2021 CPA UK has undertaken a project is entitled ‘Strengthening Democracy, Parliamentary Oversight and Sustainability in the Commonwealth.’ This is funded by the UK Government’s Foreign, Commonwealth and Development Office (FCDO) and includes workstreams on Public Accounts Committees, Women in Parliament and Climate Security. This included partially funding work on updating the Biennial Surveys for Public Accounts Committees.

Full text of the 10 Public Accounts Committee Benchmarks

- A PAC [Public Accounts Committee] should operate independently of government. PACs should have the power to select issues without government direction. The PAC’s independence should be outlined clearly through the provisions of the Standing Orders.

- PACs should have an adequate budget to cover their personnel and other operational costs, training and capacity building costs, as well as costs associated with hearings, publication of reports and sourcing external advice.

- A PAC needs non-partisan and skilled support staff. At a minimum, a PAC should have a Clerk and research staff.

- A PAC should encourage public involvement and media coverage. Committee hearings should be open to the media and the interested public, and any exceptions from this rule need to be reasonably justified.

- PAC members should have a common understanding and articulation of the PAC’s mandate, roles and powers. Members should have a good understanding of how PAC powers should be applied.

- A PAC shall have access to all records, in whatever form, to be able to scrutinise the Executive and perform the necessary oversight of public spending.

- A PAC should have the power to summon persons, papers and records, and this power shall extend to witnesses and evidence from the executive branch, including officials.

- PACs should produce a summary report of its overall findings and the extent to which its recommendations have been implemented that should lead to a debate in parliament.

- PACs need to ensure that there are robust arrangements in place to follow up their recommendations, including timelines. Such follow up may be carried out by the Supreme Audit Institution and/or the Ministry of Finance/entities concerned. However, where the PAC finds that government bodies have been slow in implementing recommendations then the senior officials of these bodies should be summoned to appear before the Committee to explain themselves.

- The Supreme Audit Institution’s independence should be firmly rooted in the Constitution or equivalent legislation which should spell out clearly the extent of its independence and powers. PACs should work to safeguard the independence of SAIs and ensure that they have the resources they need to carry out their statutory mandate.